As emissions soar, operators look to carbon capture

During 2024 and 2025, a new trend emerged: many large data center builders and operators reported increases in their Scope 2, location- and market-based greenhouse gas (GHG) emissions inventories, reversing their efforts toward net-zero commitments. While this shift does not indicate a loss of commitment to those goals, it is an inevitable result of the rapid growth in energy demand driven by data center expansion.

The International Energy Agency (IEA) and other analysts project that a menu of wind, solar, nuclear, geothermal and natural gas generation assets will be required to meet the projected 75-125 GW of new electricity demand.

- Wind and solar generation are expected to supply up to 50% of the necessary new capacity globally, with complementary battery systems to time-shift solar and wind generation from high to low output periods.

- Natural gas generation will provide a significant portion of the remaining generation capacity, as it is currently the only reliable generation type available that can be deployed on the timeline needed to meet projected demand.

- Large-scale and small modular nuclear reactors, along with geothermal generation, offer reliable, dispatchable, carbon-free generation; however, development and implementation timelines are expected to limit volume availability until the early 2030s or later.

On-site and grid-connected natural gas generation will play a significant role as the primary generation source for many planned data center campuses, as well as acting as “fill-in” generation assets to stabilize the grid during periods of low wind and solar output. As a result, data center operators will face a choice: access or deploy these generation assets with carbon capture and storage (CCS) systems or delay their facility-specific net-zero carbon goals to 2040 and beyond.

Carbon capture technologies are still immature; however, turbine manufacturers are offering natural gas combined cycle (NGCC) and simple cycle turbines integrated with commercially available amine-based solvent CCS systems. Several projects are underway to construct and operate natural gas electricity generation systems with CCS. But the use of this technology will depend on the ability to colocate with carbon storage facilities — and on economics.

It is widely expected that carbon capture will become more competitive as the cost of offsets increases. While CCS is expected to add 10-30% to the cost of electricity, Uptime Intelligence estimates that this premium will soon be comparable to the cost of energy attribute certificates (EACs) and carbon offsets currently applied by operators to achieve market-based net-zero emissions goals.

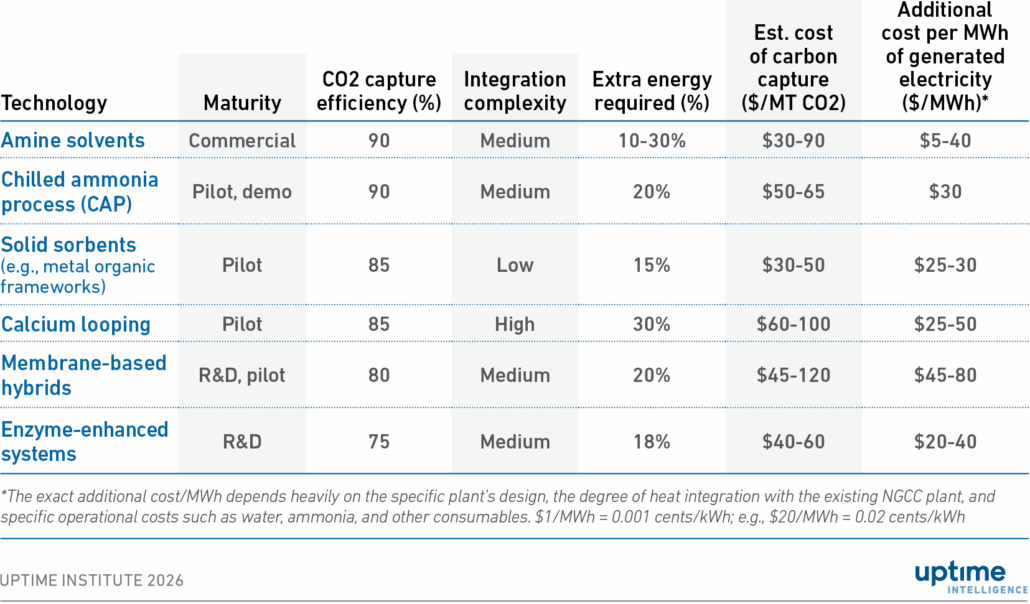

Carbon capture technologies

Carbon capture is no longer a new technology, but its use has been very limited due to the difficulty of securing carbon storage capacity and by the additional capital and operating costs involved. However, the key role of natural gas-fired electricity generation in powering the planned data center build-out, combined with the need to decarbonize the data center energy supply to meet GHG reduction commitments, may necessitate greater deployment.

There are six distinct carbon capture technologies available (see Table 1). Of these, only the amine solvent systems are currently commercially available. Of the remaining five, solid sorbent and chilled ammonia technologies appear the most promising, as they most easily integrate with an NGCC system, have lower energy debt, lower costs per metric ton of removal and per MWh generated, and are further along in the development process. Nevertheless, all five non-commercial technologies will require at least five years of pilot and demonstration projects to validate their technical and economic credentials.

Table 1 Carbon capture technologies

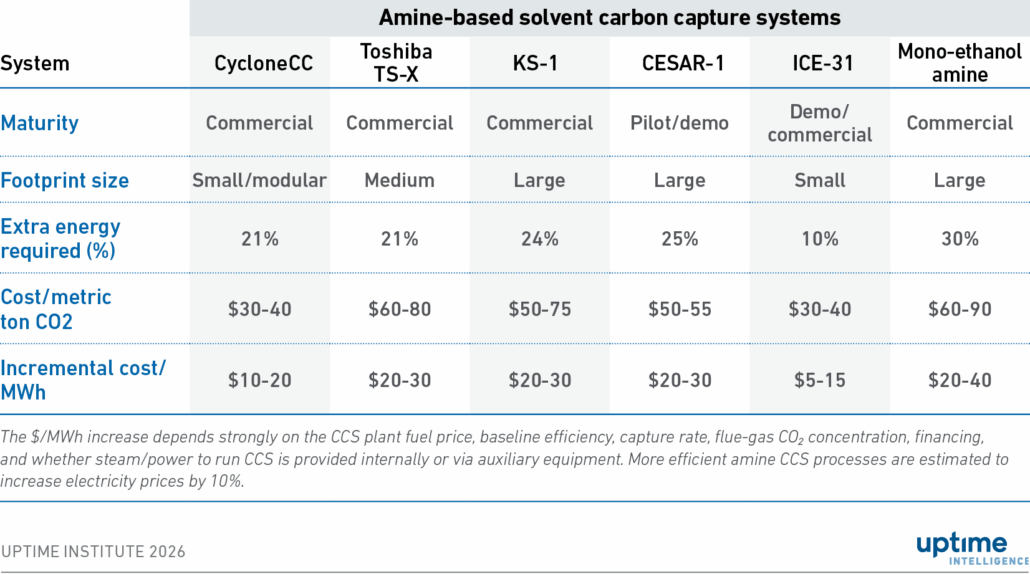

Amine-based CCS systems

Amine-based CCS systems are installed and operating at facilities with CO2 flue gas concentrations of 15% or more, such as coal-fired electricity generation assets and fertilizer and chemical manufacturing plants. While they have not yet been deployed at a commercial scale on natural gas-powered electricity generation assets, their application is technically feasible. Pilot and demonstration projects using natural gas turbines, which have CO2 flue gas concentrations of 4-7%, have indicated that CO2 can be captured at up to 90% efficiency.

There are six types of amine-based carbon capture systems currently available (see Table 2). These systems differ in both the cost per metric ton of CO2 removal and the cost per generated MWh. Still, the premium for carbon capture systems will likely be 10-40% of the electricity costs, depending on fuel prices, CO2 concentration in the flue gas, and the type and source of the energy consumed for CCS operation and capture media regeneration.

Table 2 Amine-based carbon capture systems

An 860 MW natural gas combined cycle (NGCC) power plant with an integrated amine-based CCS system (supplied by GE Vernova), currently under construction in Teesside, UK, will be the first full-scale CCS deployment on an electricity-generating asset. The facility is colocated with a North Sea carbon storage facility. It is expected to enter operation in 2026 and remove 2 million metric tons of CO2 per year.

CCS opportunities and challenges

Recent announcements by hyperscalers indicate growing activity in NGCC/CCS systems. Google has entered into a power purchase agreement (PPA) with a 400 MW integrated natural gas-fired cogeneration and CCS plant in Illinois. Microsoft has publicly expressed openness to procuring electricity from natural gas-fired power plants with CCS when it is economically viable.

Energy developers and turbine generator manufacturers are also entering the market with a specific focus on data center operators. ExxonMobil/NextEra and Chevron are involved in the development and marketing of data center campuses with behind-the-meter NGCC/CCS generation. GE Vernova and Engine No. 1 have co-developed and are marketing an integrated natural gas turbine/CCS offering for behind-the-meter use in data centers.

CCS systems perform best on natural gas generation assets that operate continuously; therefore, they will not be suitable for standby generation. They are appropriate for behind-the-meter or on-grid power generation assets.

Constructing an integrated NGCC/CCS system can take up to two years longer than constructing a standalone NGCC system. Given the urgency of installing new generation capacity to support planned data center builds, carbon capture systems will likely go into operation two or three years after the NGCC system, improving the overall energy delivery timeline.

Carbon transport and storage

The viability of a carbon capture project depends on the availability of an accessible, permitted geological formation capable of storing carbon. As a result, operators will need to locate data centers in electricity grid regions with carbon storage facilities — such as Texas, the North Sea, the Santos pre-salt basin in Brazil, Gorgon in Australia, Qilu-Shengli in China — or colocate with a carbon storage facility or pipeline to access low-carbon, natural gas-generated electricity. This limitation will rule out retrofitting CCS systems to existing generation capacity and require operators to partner with energy developers with CCS expertise for new generation.

CO2 can be stored in four different types of geological formations:

- Oil and gas reservoirs. Depleted oil and gas reservoirs can store CO2. In some cases, CO2 injection has the added benefit of improving oil extraction from the rock formation. Oil fields have been injecting and storing CO2 for more than 30 years.

- Deep saline formations. These porous rock formations are found in many areas worldwide and are projected to be capable of sequestering thousands of gigatonnes of CO2. Suitable formations must be at least 800 meters below the surface and overlain by impermeable cap rock such as shale.

- Coal beds. Coal beds that are too deep or too thin to be economically mined may have potential for CO2 storage.

- Basalt formations and shale basins. CO2 can be captured in both basalt and shale formations. In basalt formations, CO2 has been shown to mineralize over time. A small demonstration project is underway at a basalt formation in Iceland; however, neither type of formation has been tapped for commercial, high-volume carbon storage.

The CO2 transport and injection/monitoring processes add $10-30 per metric ton of CO2 stored and $5-15 per MWh. These factors are included in the cost per metric ton of captured CO2 values in Tables 1 and 2.

The amount that data center operators pay for power varies widely, however, Uptime Intelligence estimates that CCS systems — including generation/carbon capture with storage — will increase electricity costs by 15-40% at $70 per MWh and 10-25% at $140 per MWh. One source estimates that CCS systems will have a premium of $25-50 per MWh. As most systems are still in the research and development, pilot and demonstration phases, the final costs of carbon capture remain highly uncertain. They are expected to decline as experience is gained from early, full-scale systems.

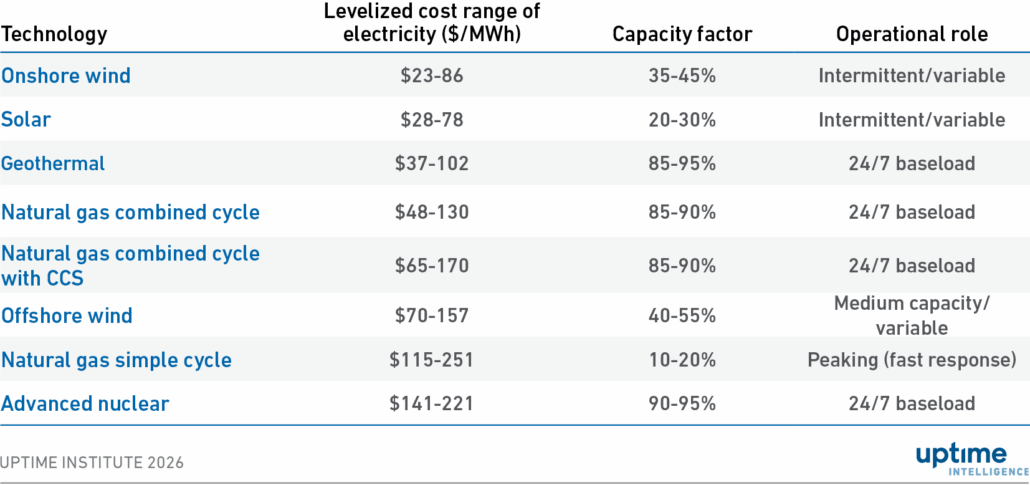

The cost of electricity from NGCC/CCS systems is competitive with the other baseload technologies. Although wind and solar generation can have much lower costs, additional investments in batteries and/or baseload or peaking power are required to provide reliable power to the grid, increasing the cost per MWh into a range comparable with NGCC/CCS generation (see Table 3). Electricity costs will vary by region and over time based on fuel prices, financing and capital costs, and the complexity and duration of the permitting process.

Table 3 Levelized cost of electricity by generation technology

Net-zero goals need carbon capture

Many data center operators have set net-zero CO2e emissions goals for their businesses. Given the planned power demand of the data center build-out, natural gas electricity generation assets will be a critical component of the industry’s electricity supply strategy. Operators will need to procure electricity from NGCC/CCS generation facilities to meet net-zero goals at the facility level.

With an estimated energy price premium of 10-20%, NGCC/CCS systems offer a viable alternative to virtual power purchase agreements (VPPA) and their associated energy attribute certificates (EACs), as well as to forestry, soil and direct air capture projects. The cost of a VPPA-based EAC is often opaque, as it depends on the VPPA electricity cost and the average spot market price for the generation region. As such, the cost of an EAC can reflect either the loss or profit of the energy purchase contract. By comparison, soil and forestry carbon offsets currently cost $10-50 per metric ton of carbon, and direct air capture offsets cost $600-1,000 per metric ton. Capturing carbon at its source of generation offers a viable strategy from both a cost-management and public-relations perspective.

Note: EACs represent the zero-emissions characteristics of carbon-free electricity generation.

To demonstrate their commitment to their net-zero plans, operators will need to work with energy developers and turbine manufacturers to deploy natural gas generation with CCS as part of their data center build-out plans. Given the economic realities of the EAC and carbon offset markets, these systems can be financially attractive while directly reducing CO2 emissions associated with the operation of their data center facilities.

The Uptime Intelligence View

The rapid expansion of the global data center footprint, and the associated growth in power demand, will necessitate the deployment of gigawatts of natural gas generation. Without carbon capture, the deployment and use of these generation systems will significantly increase facility-level Scope 1 and Scope 2 emissions, pushing operators’ net-zero commitments to 2040 or beyond.

Where operators can purchase electricity from NGCC/CCS assets, they should be able to source low-carbon power at prices that are competitive with other carbon-free energy alternatives. This option will not be viable in many markets due to the unavailability of storage capacity, and operators will therefore need to develop partnerships with energy developers that specialize in NGCC/CCS systems in markets where storage is available. Nevertheless, operators that are serious about their net-zero commitments will need to support development of CCS technologies, include access to these systems in their site selection process, and procure low-carbon energy generated from these systems where it fits with business and sustainability objectives.

The post As emissions soar, operators look to carbon capture appeared first on Uptime Institute Blog.