Data Center Liquid Cooling Market to Surpass USD 27.1 Billion by 2035

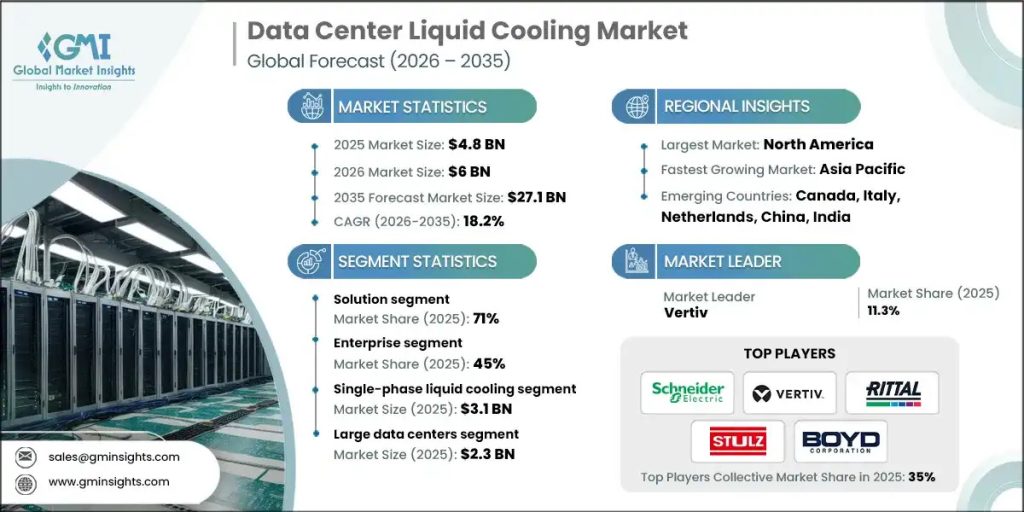

The global data center liquid cooling market was valued at USD 4.8 billion in 2025 and is estimated to grow at a CAGR of 18.2% to reach USD 27.1 billion by 2035, according to a recent report by Global Market Insights Inc.

Rising energy costs, coupled with stringent sustainability requirements, are accelerating the adoption of liquid cooling technologies across data centers. Liquid cooling systems offer significantly lower Power Usage Effectiveness (PUE) ratios ranging from 1.05 to 1.15 compared to 1.4-1.8 for traditional air-cooled facilities, which directly lowers electricity consumption and reduces carbon emissions. Regulatory mandates, including the EU Energy Efficiency Directive, Germany’s Energy Efficiency Act targeting PUE 1.3 by 2027, and California’s energy efficiency standards, are pushing operators toward advanced cooling solutions.

Furthermore, the ability of liquid cooling systems to recover waste heat for district heating or industrial processes transforms data centers into contributors to circular energy economies, supporting corporate net-zero initiatives and enhancing operational sustainability. North America continues to lead the data center liquid cooling market, driven by a dense concentration of hyperscale cloud operators, semiconductor manufacturers, and systems integrators deploying high-density AI and HPC infrastructure.

The solution segment held a 71% share in 2025 and is forecast to grow at a CAGR of 15% from 2026 to 2035. Direct-to-chip cooling is the fastest-growing technology, employing cold plates and micro-channel coolers attached directly to processors, GPUs, and memory to remove 60-80% of heat before it enters the air. These systems circulate coolants such as water with inhibitors or glycol mixtures across chip surfaces, achieving thermal resistances as low as 0.01-0.05°C/W.

The single-phase liquid cooling systems segment reached USD 3.1 billion in 2025. These systems maintain coolant in liquid form throughout the cycle, transferring heat via conduction and convection without phase change. Coolants circulate through cold plates, immersion tanks, or heat exchangers at 18-50°C, depending on design, while facility chillers, dry coolers, or towers remove heat from the loop.

U.S. data center liquid cooling market captured USD 1.29 billion in 2025. Federal initiatives, including AI and HPC programs, semiconductor funding under the CHIPS Act, and defense modernization projects incorporating AI, are key drivers of liquid cooling adoption in public sector data centers.

Leading companies in the data center liquid cooling market include Alfa Laval, Asetek, Boyd, CoolIT Systems, Green Revolution Cooling, LiquidStack, Rittal, Schneider Electric (Motivair), Stulz, and Vertiv. Key strategies adopted by companies in the market focus on technological innovation, such as developing high-efficiency immersion and direct-to-chip cooling solutions for next-generation processors and GPUs. Firms are forming strategic partnerships with hyperscale cloud providers, semiconductor manufacturers, and HPC integrators to expand deployment. Investments in R&D for energy-efficient, modular, and scalable systems strengthen product differentiation. Companies are also emphasizing geographic expansion into emerging markets, supporting sustainability initiatives, and integrating IoT-enabled monitoring tools to optimize performance, enhance reliability, and maintain long-term client relationships.

The post Data Center Liquid Cooling Market to Surpass USD 27.1 Billion by 2035 appeared first on Data Center POST.